DI - 01: Korean CEX

Korean Centralized Exchanges and Investors' Behavior Through Data

1. Introduction

In Data Insight, we provide insights on specific topics through data analysis. For this article, we have chosen Korean centralized exchanges as the theme to explore. According to a survey by the Korea Financial Intelligence Unit (KoFIU), the number of crypto investors in Korea is expected to reach approximately 6 million in the first half of 2023, which is an astonishing figure accounting for over 10% of the total population of South Korea. However, the majority of these investors are primarily engaged in investment activities centered around centralized exchanges, making the influence of centralized exchanges in the Korean crypto market significant.

In the following sections, we will examine the data of Korean centralized exchanges and explore the characteristics and tendencies of Korean investors. The analysis is mainly based on the data from the four major exchanges: Upbit, Bithumb, Coinone, and Korbit. Some analysis is based on data from the third week of October (14th to 20th).

2. Increase in the Share of Korean Exchange Trading Volume Despite Overall Decrease

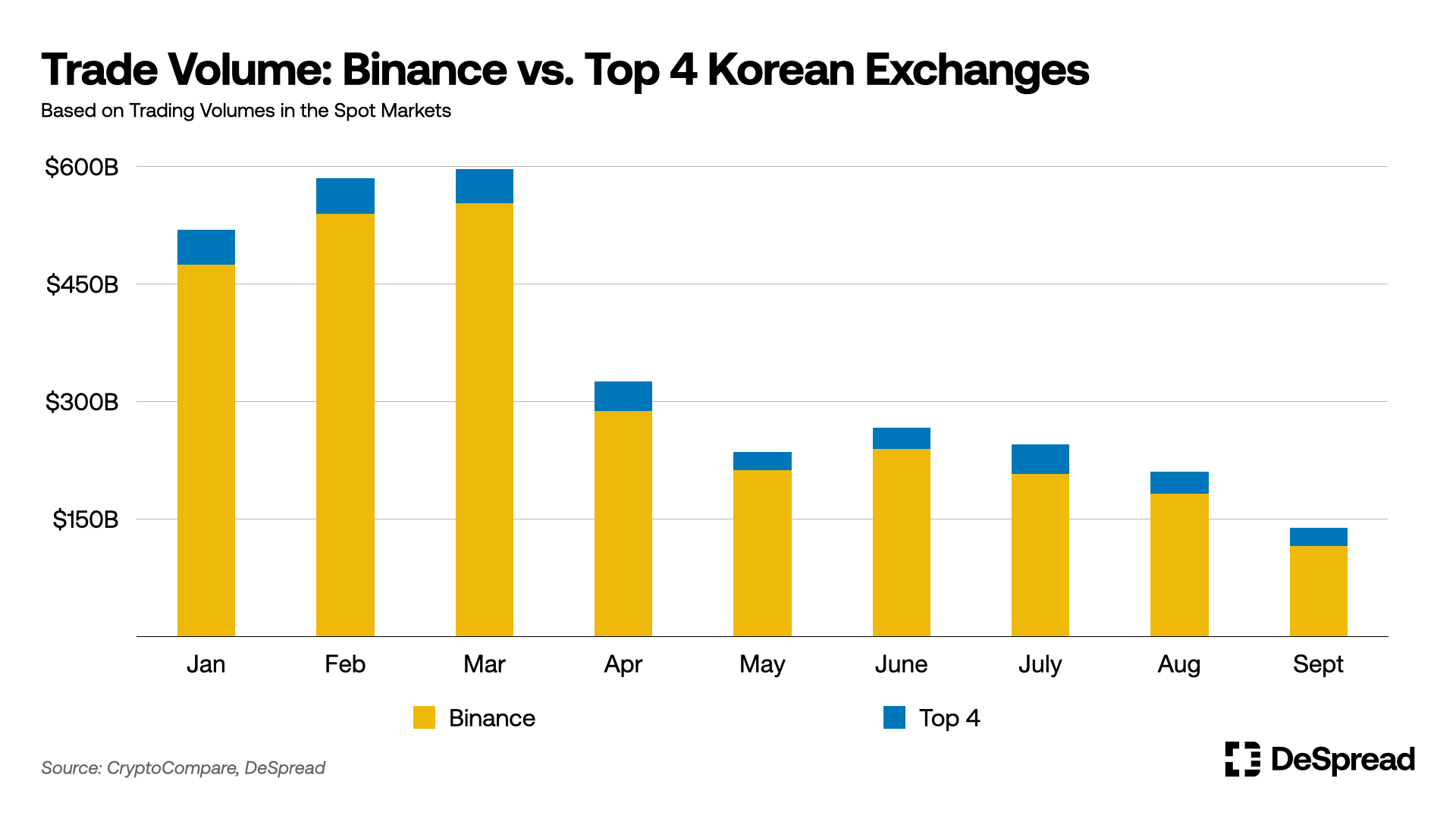

- Decreasing trading volume trend: The trading volume of centralized exchanges (CEX) has shown a decreasing trend overall since reaching its peak in March this year. During this period, market volatility also decreased, and the price of Bitcoin remained relatively stable at around $27K to $28K from the end of March to the end of September without significant fluctuations for six months.

- Relative strength of Korean exchanges: Korean exchanges were not an exception to this contraction trend. After reaching a peak of $45B in total trading volume in February, the volume sharply declined to $23B in May. However, it showed an upward trend thereafter, recording a trading volume of up to $37B in July, demonstrating a larger increase compared to Binance, the world's largest cryptocurrency exchange.

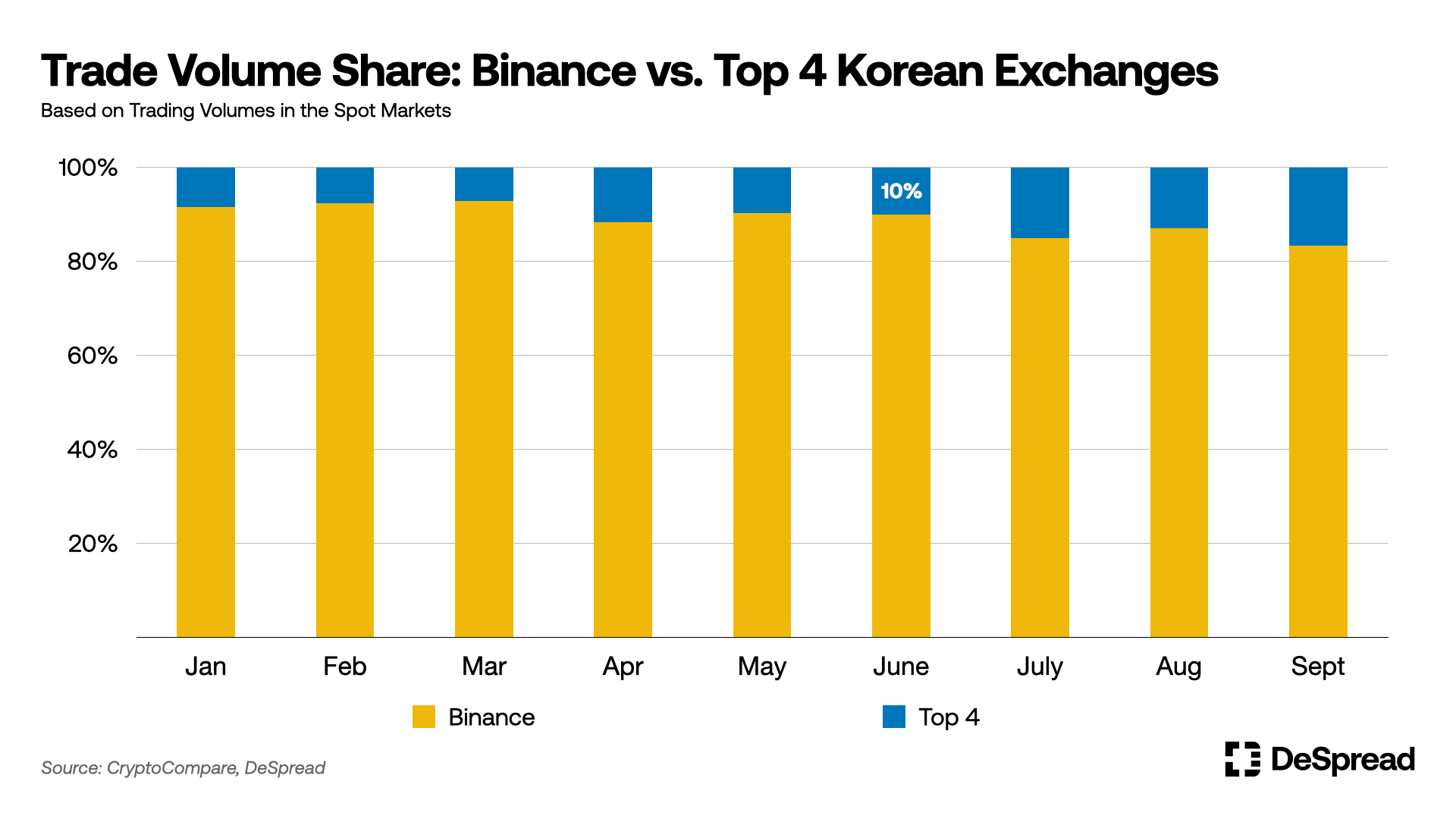

- Position of Korean exchanges compared to international exchanges: In comparison analysis with Binance, the four major Korean exchanges showed a trading volume at around 10% level compared to Binance this year. Particularly, when compared to Coinbase during the same period, they recorded higher trading volumes, indicating that Korean exchanges have a significant presence in the international market.

- Increasing market share trend: Additionally, the market share of the four major Korean exchanges has been consistently increasing. The trading volume relative to Binance increased from 7% in March to 16% in September. This can be interpreted as an indicator reflecting the increased influence of domestic exchanges.

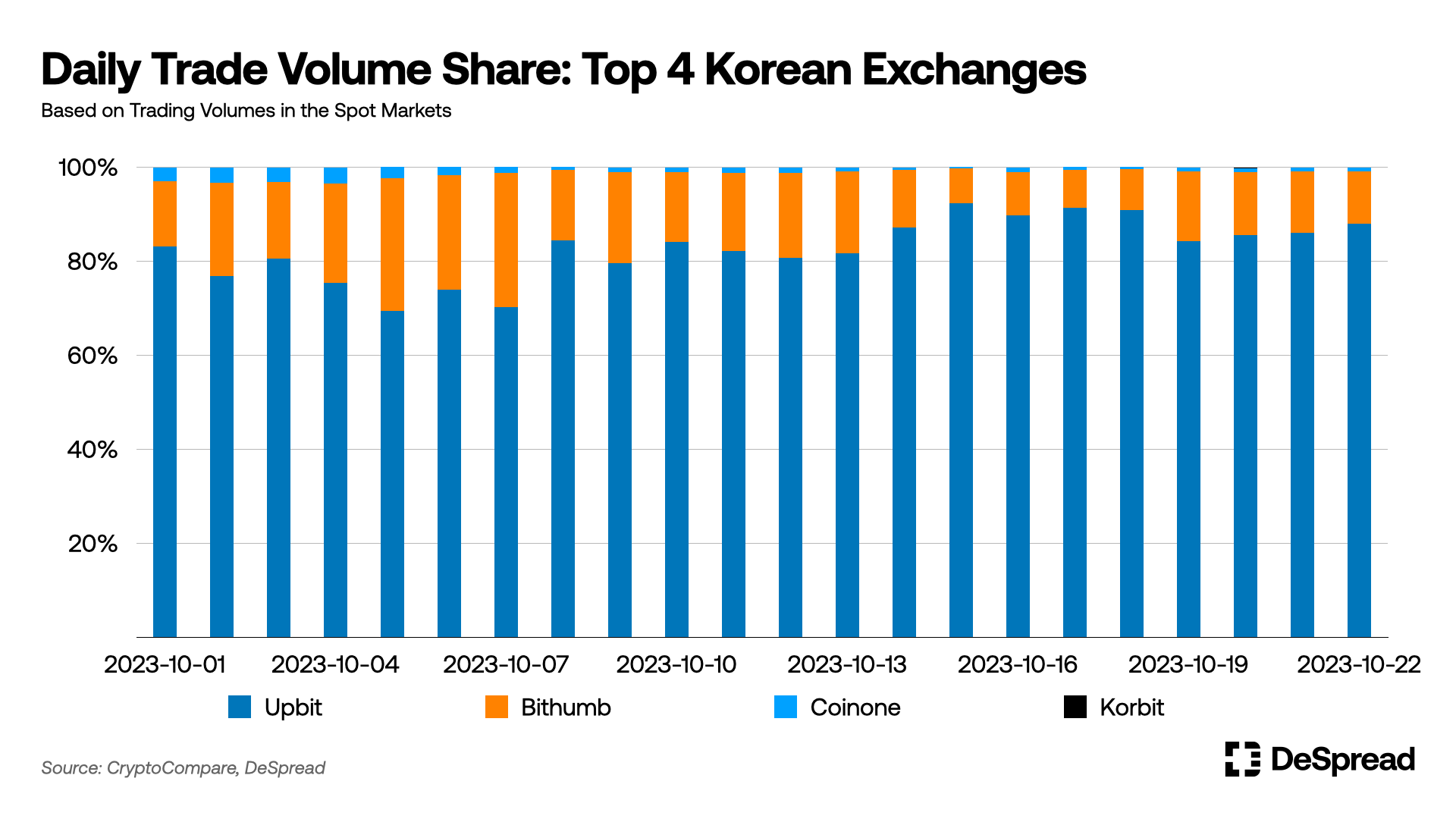

3. The Upbit Monopoly

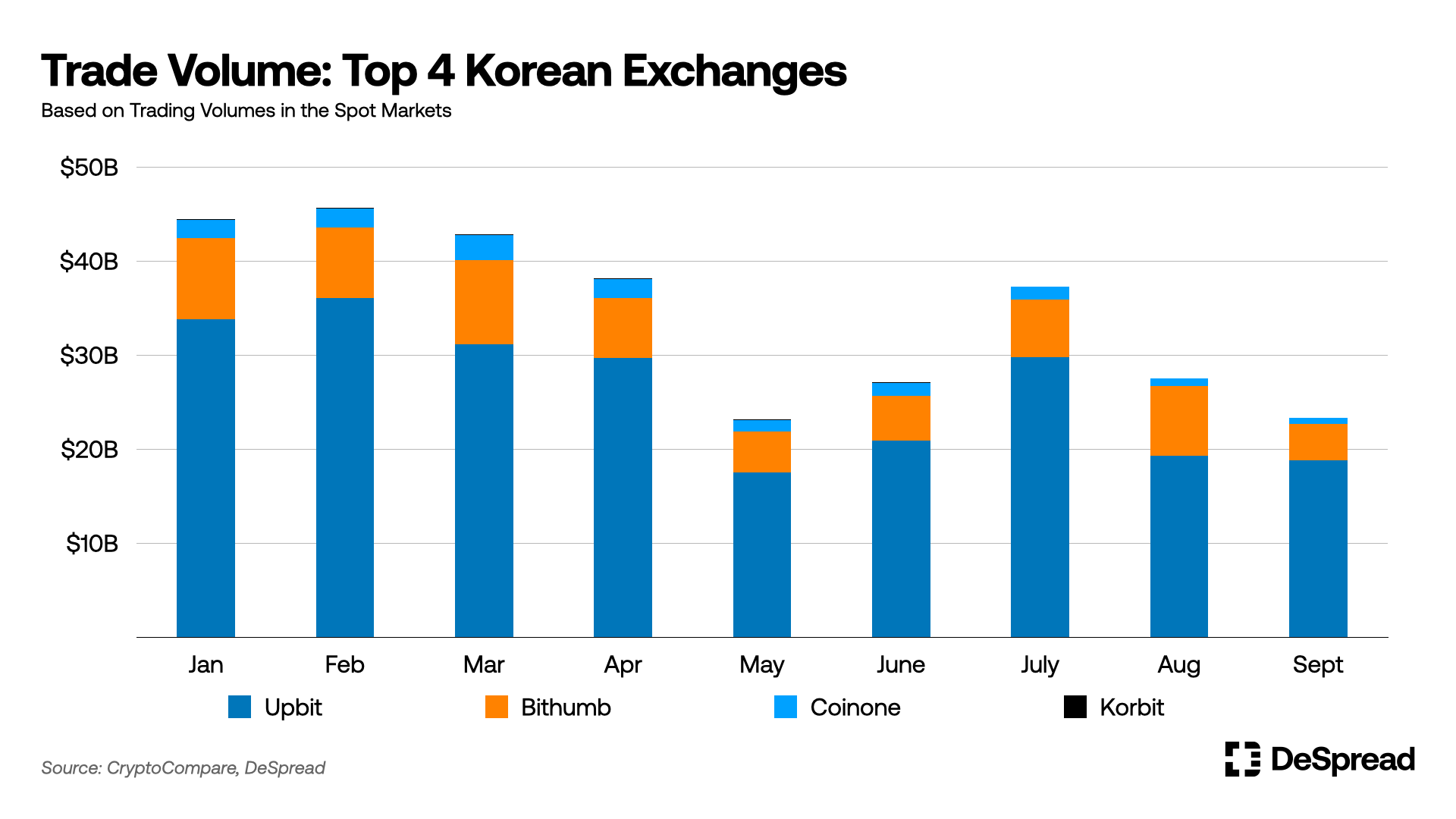

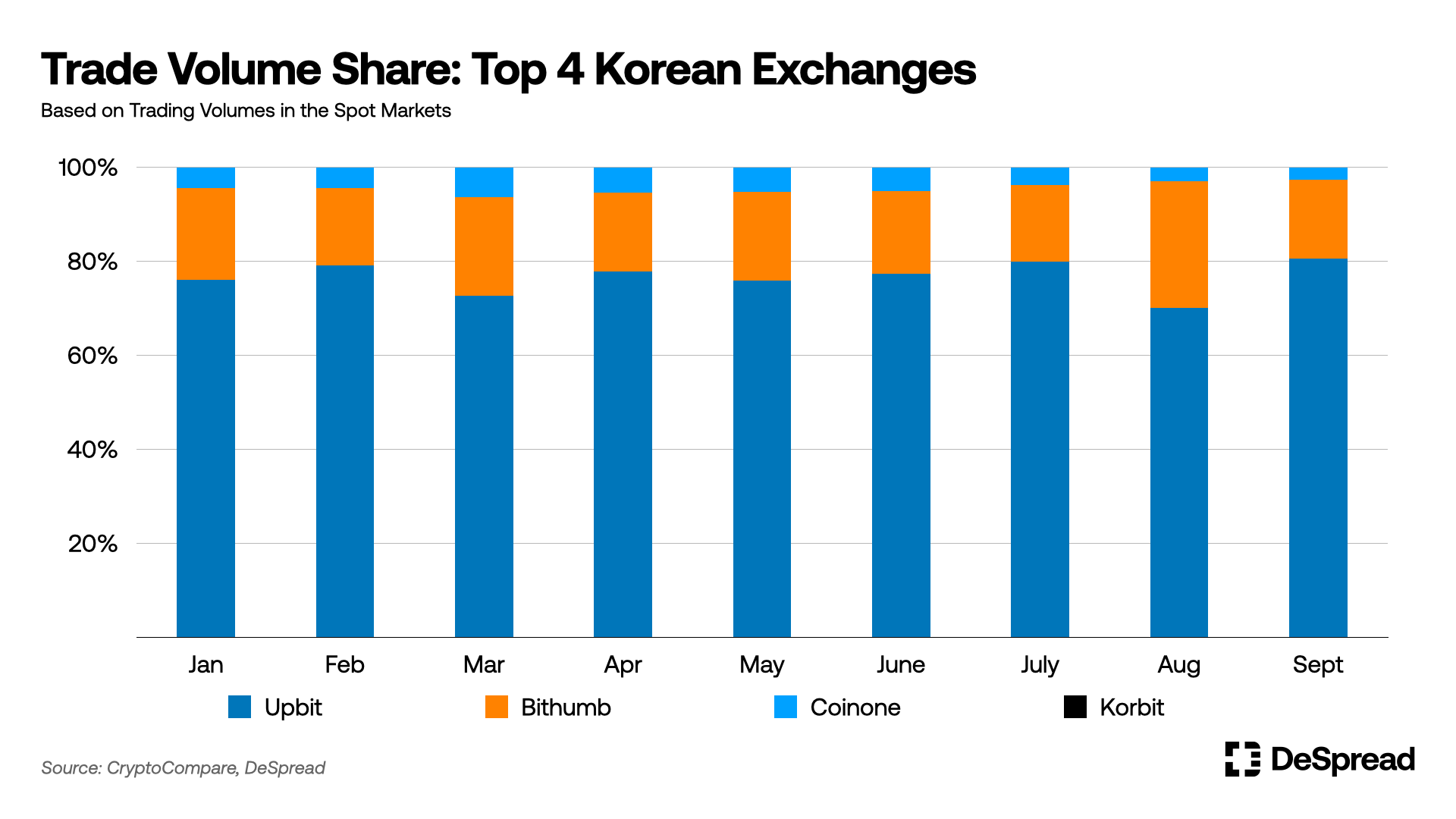

- Upbit crushing competition: In February of this year, Upbit recorded its highest trading volume of $36 billion, accounting for about 80% of the Korean crypto exchange market, maintaining a dominant position. Although its market share briefly dropped to 70% in August, it quickly rebounded to 80% the following month, showing a consistent trend in market share.

- Market share of Bithumb, Coinone, and Korbit: Bithumb maintains a strong position as the second-largest player in the market, accounting for 15% to 20% of the total trading volume among the four major exchanges. On the other hand, Coinone has a market share between 3% and 5%, and Korbit has a share of less than 1%, indicating relatively limited market share.

- Korea's enthusiastic response to the Ripple ruling: While Binance did not show significant volatility in trading volume in July compared to the previous month, Korean exchanges had an explosive reaction to news related to Ripple. The trading volume of the four major Korean exchanges, which recorded $27 billion in June, increased to $37 billion in July, a 37% increase from the previous month. This was mainly due to the news of Ripple's partial victory in the lawsuit with the SEC, which led to an 80% surge in XRP prices and a sharp increase in trading volume on July 13.

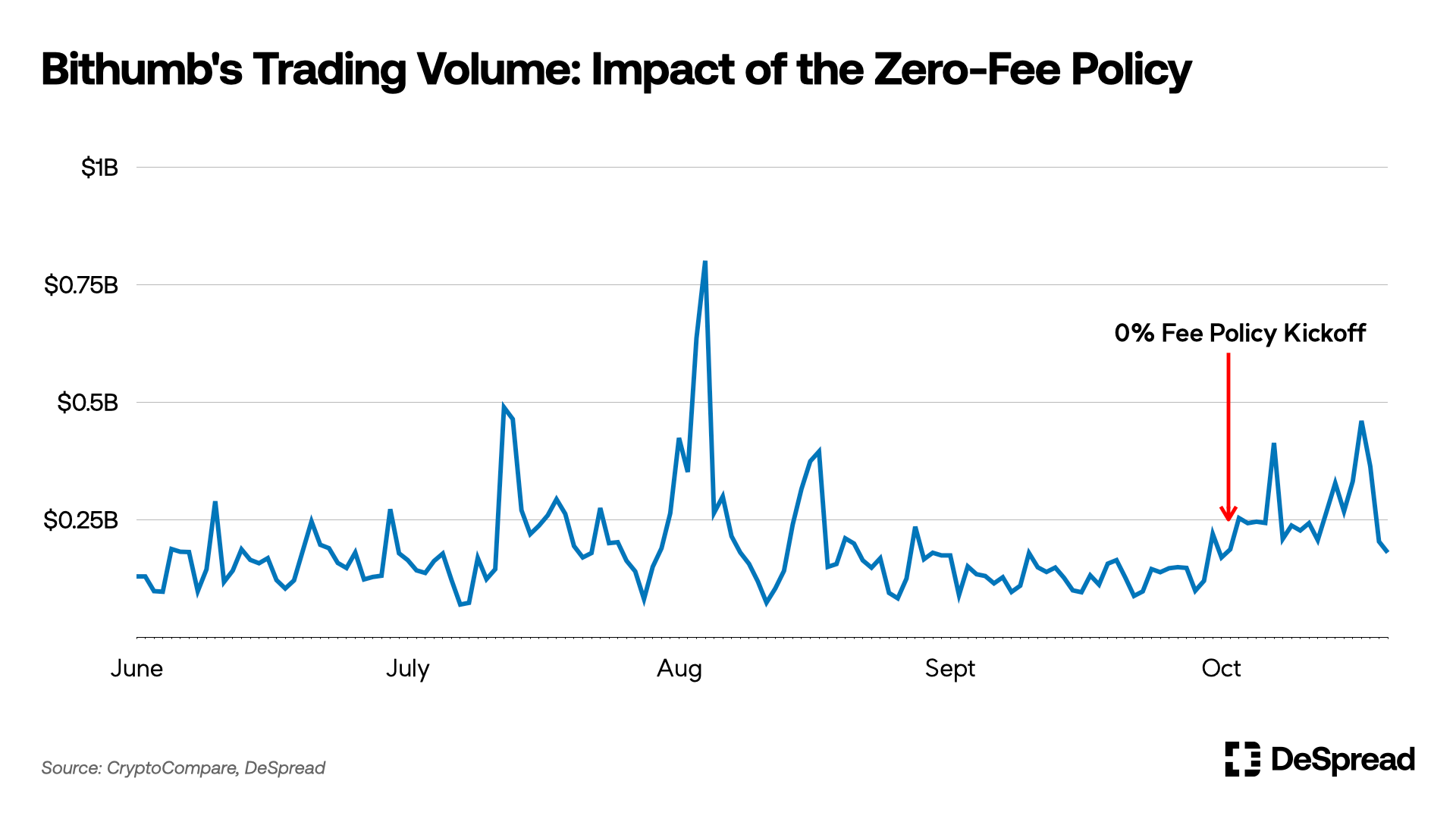

4. Bithumb's Zero-Fee Policy

- Initial response to zero-fee policy: Bithumb, the second largest exchange in South Korea, implemented a 0% fee policy on October 4th. This policy initially had a positive effect, as Bithumb's trading volume increased and its market share exceeded 20%.

- Declining market share: However, the impact of the fee exemption policy did not last long, and Bithumb's market share declined, returning to pre-policy levels.

- Sustainability of zero-fee policy: While Bithumb's fee exemption policy was effective in increasing market share initially, it is uncertain whether it can sustainably grow the exchange in the long term. This also indicates that Korean investors' choice of exchange is not solely based on the presence or absence of fees. Furthermore, there are concerns about the sustainability of this policy, as it eliminates a major source of revenue for the exchange.

5. Coinbase and Upbit

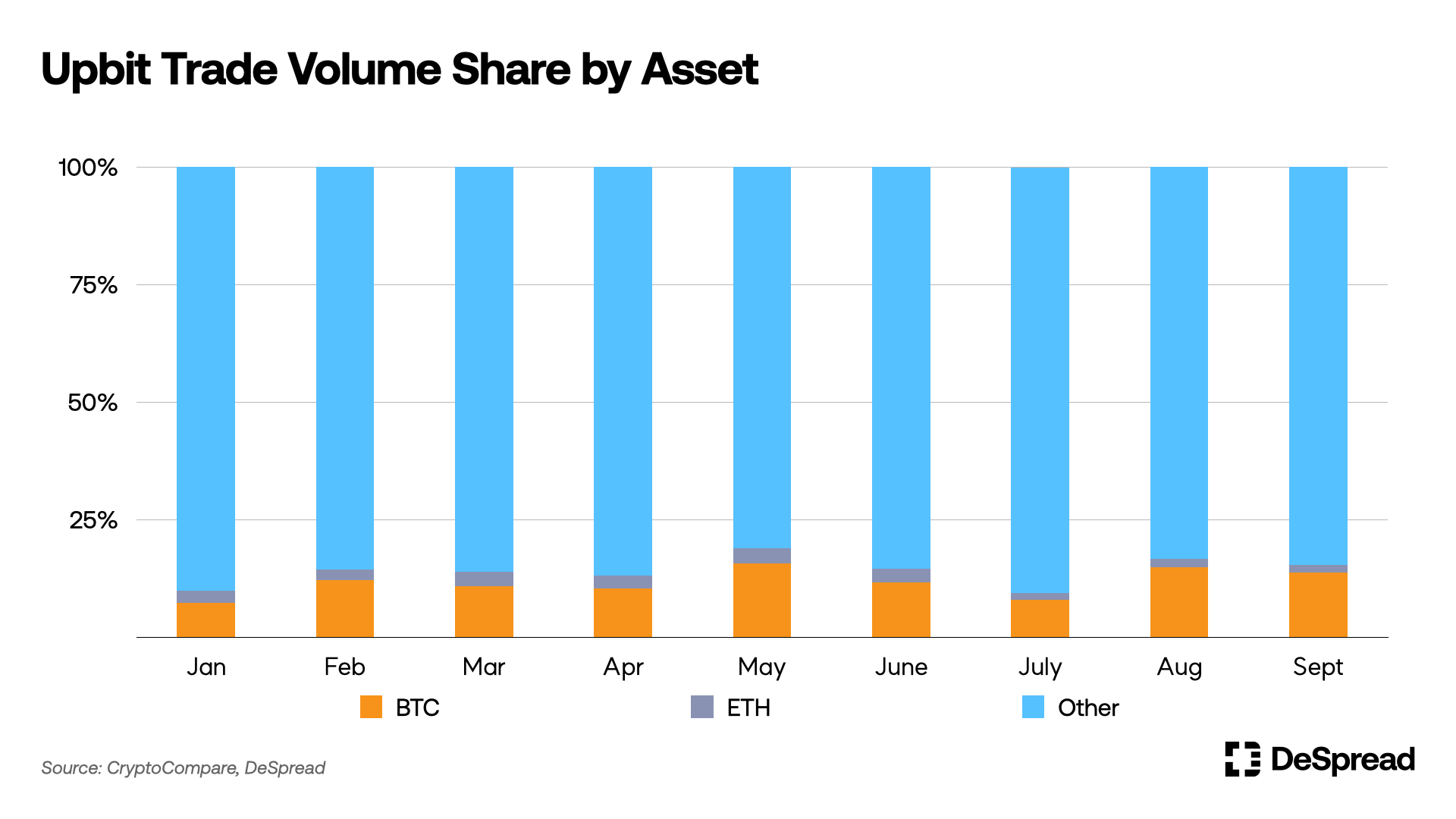

- High-risk, high-reward investment style: Upbit, while BTC and ETH trading volumes account for a small portion of the total trading volume, Coinbase, a representative cryptocurrency exchange in the United States, has a significant proportion of trading volume in these two cryptocurrencies. The majority of individual investors on Upbit show strong interest in altcoins with high profit potential and tend to accept the associated high risks. This is considered one of the reasons for the high proportion of altcoin trading in the Korean market.

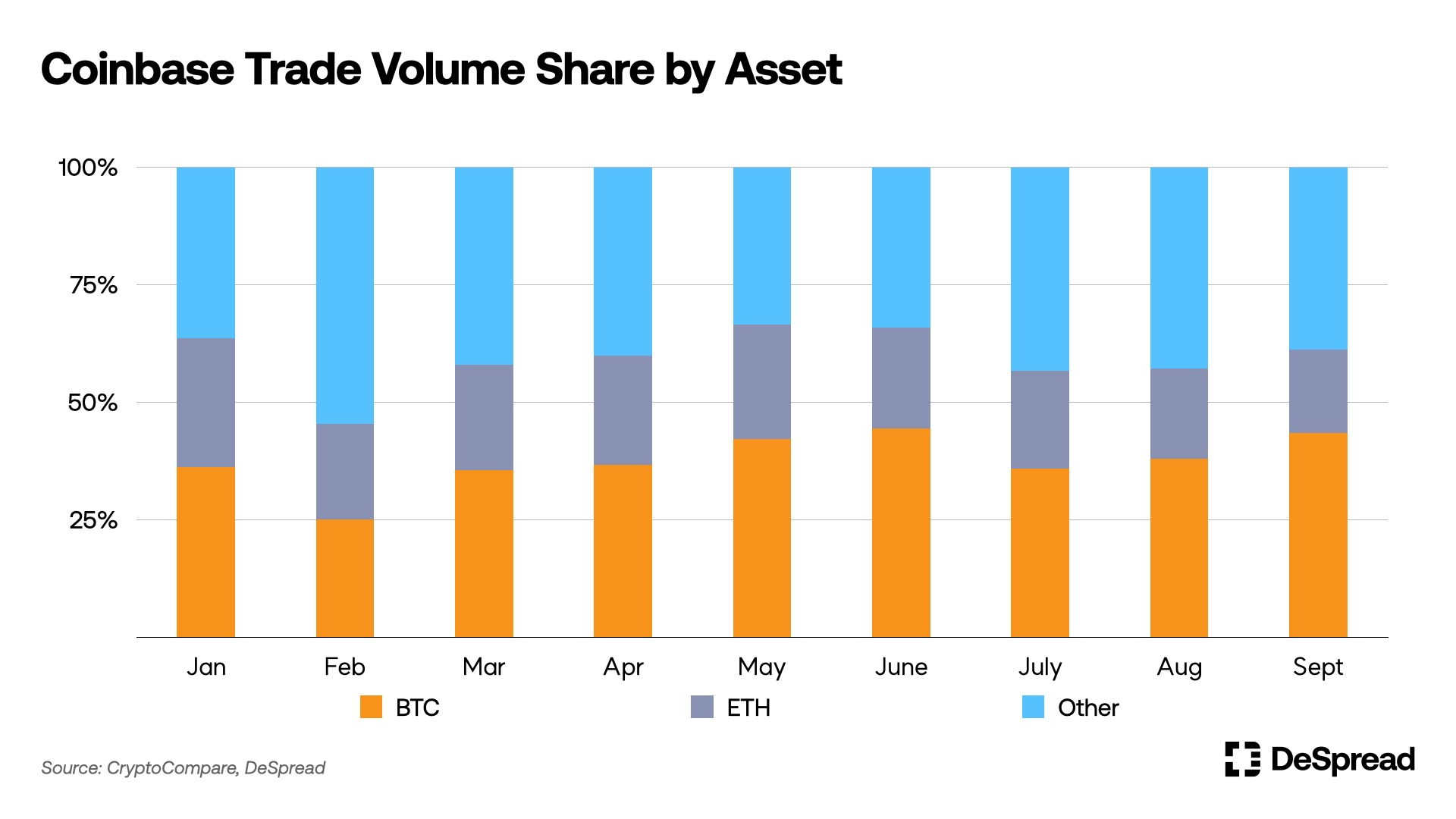

- Institutional investor-centric trading: Unlike Upbit, where individual investors dominate, Coinbase's trading volume is driven by institutional investors. According to Coinbase's Q2 shareholder letter, institutional investors account for approximately 85% of Coinbase's total trading volume. They tend to pursue portfolio stability, which is why trading in BTC and ETH, which boast the highest market capitalization among cryptocurrencies, occupies a relatively high proportion.

6. Characteristics of the Korean Market

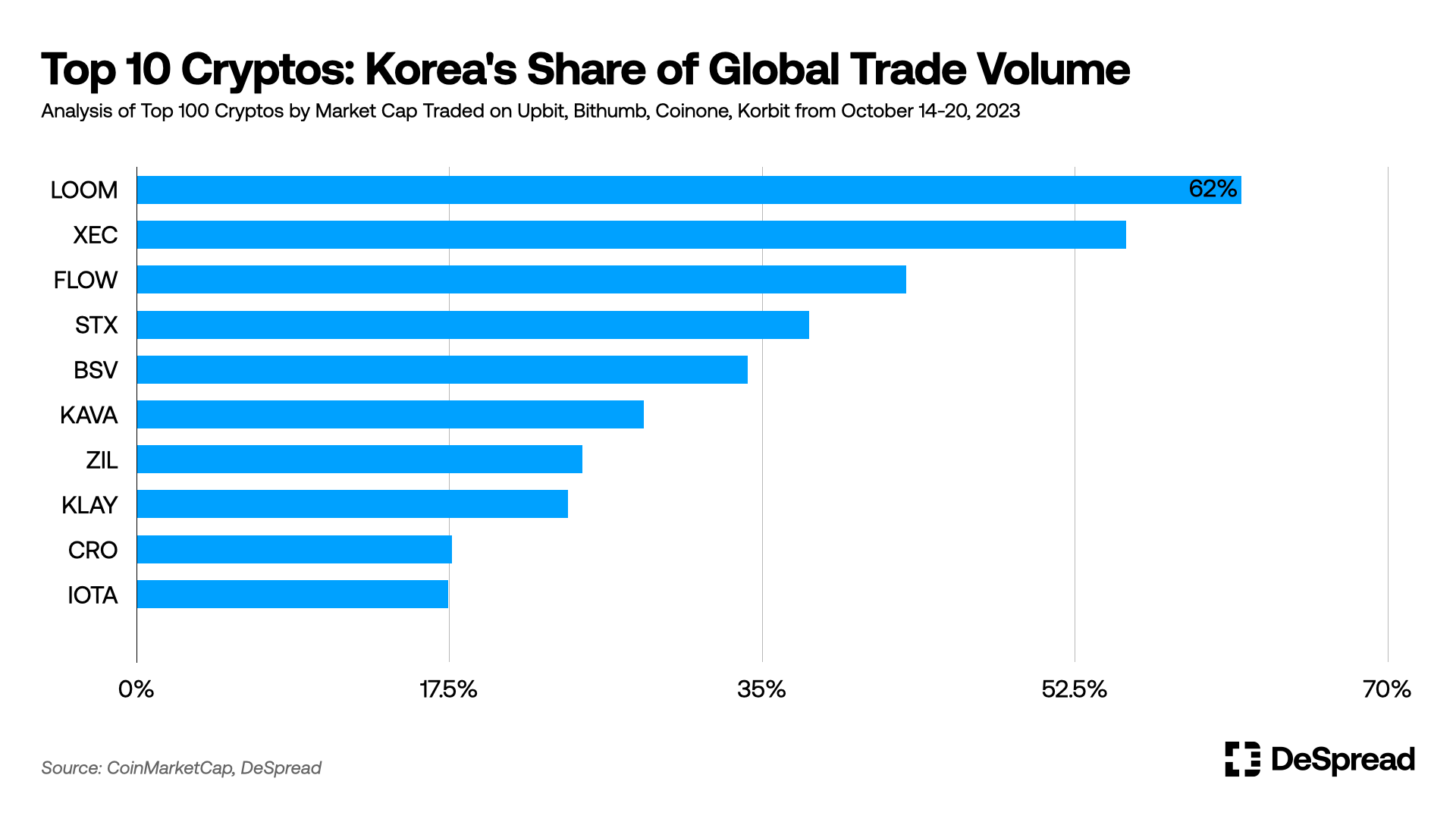

- Coins favored by Korean investors: The chart above provides a glimpse of which coins Korean investors are primarily interested in. Analyzing data on cryptocurrencies that were most actively traded in Korea compared to the global market last week, we found that Loom Network ($LOOM) recorded the highest trading volume with a ratio of 62%, claiming the top spot. This was followed by eCash ($XEC) with 55% and Flow ($FLOW) with 43%. Stacks ($STX) and Bitcoin SV ($BSV) also made it to the rankings with ratios of 37% and 34% respectively.

- Surging $LOOM, Mysterious Moves: In the third week of October, when compared to the global market, the most actively traded cryptocurrency in Korea was Loom Network ($LOOM). This means that Korean investors were actively trading this asset compared to global investors. Starting from September 15th, the token price began to rise without any specific reason and skyrocketed nearly 10 times in just one month, reaching ₩686. However, starting from October 15th, it began to plummet and currently sits at around ₩140 while writing this report. Due to such drastic price fluctuations, Loom Network briefly entered the top 100 global market cap rankings.

- Impact of exchange deposit and withdrawal policies: Changes in deposit and withdrawal policies by Korean exchanges can have a direct impact on prices and trading volumes. Specifically, on October 14th, $FLOW experienced a pattern of significant price and trading volume increases compared to the previous day when deposits and withdrawals were temporarily suspended. This phenomenon, known as the "가두리(Gaduri)" effect, occurs when arbitrage trading with overseas exchanges becomes impossible due to the suspension of deposits and withdrawals.

- Coins receiving steady attention: While there are cryptocurrencies that receive temporary attention, such as Loom Network and Flow, cases like Stacks and eCash continue to receive consistent attention on Korean exchanges regardless of temporary events. These cases are noteworthy as they are consistently traded in the Korean market regardless of global trends.

7. In-depth Analysis of Upbit Investors

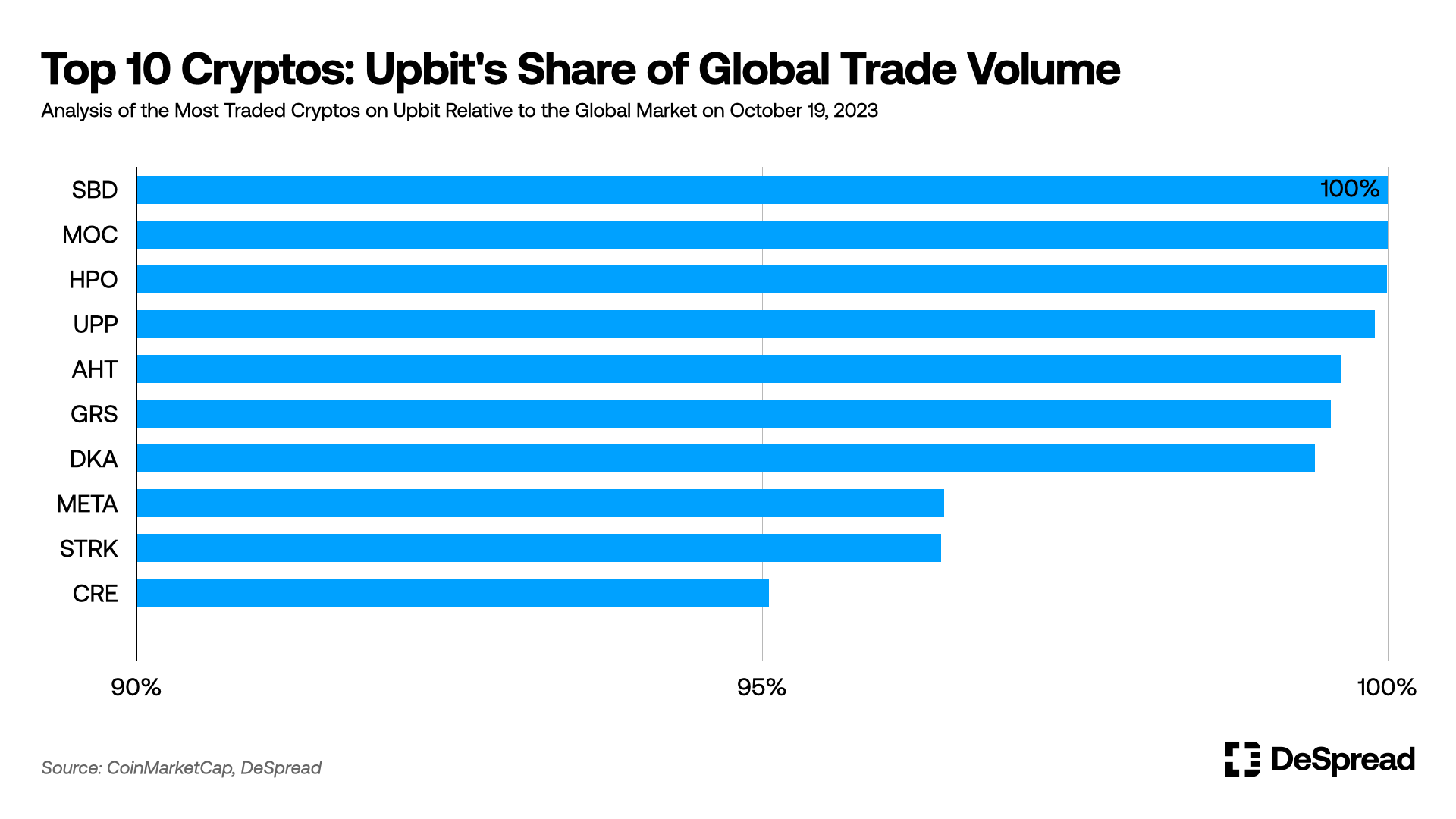

- “Kimchi Coins” mainly traded on Upbit: Among the cryptocurrencies traded on Upbit, Steem Dollars ($SBD), Moss Coin ($MOC), and Hippocrat ($HPO) account for 100% of the trading volume and are traded exclusively on Upbit. In addition, cryptocurrencies such as Sentinel Protocol ($UPP), Aha Token ($AHT), and Groestlcoin ($GRS) are mainly traded on Upbit and are referred to as Kimchi Coins as they do not receive much attention in the global market. These coins are predominantly traded by Korean investors and form their own market within the Upbit platform.

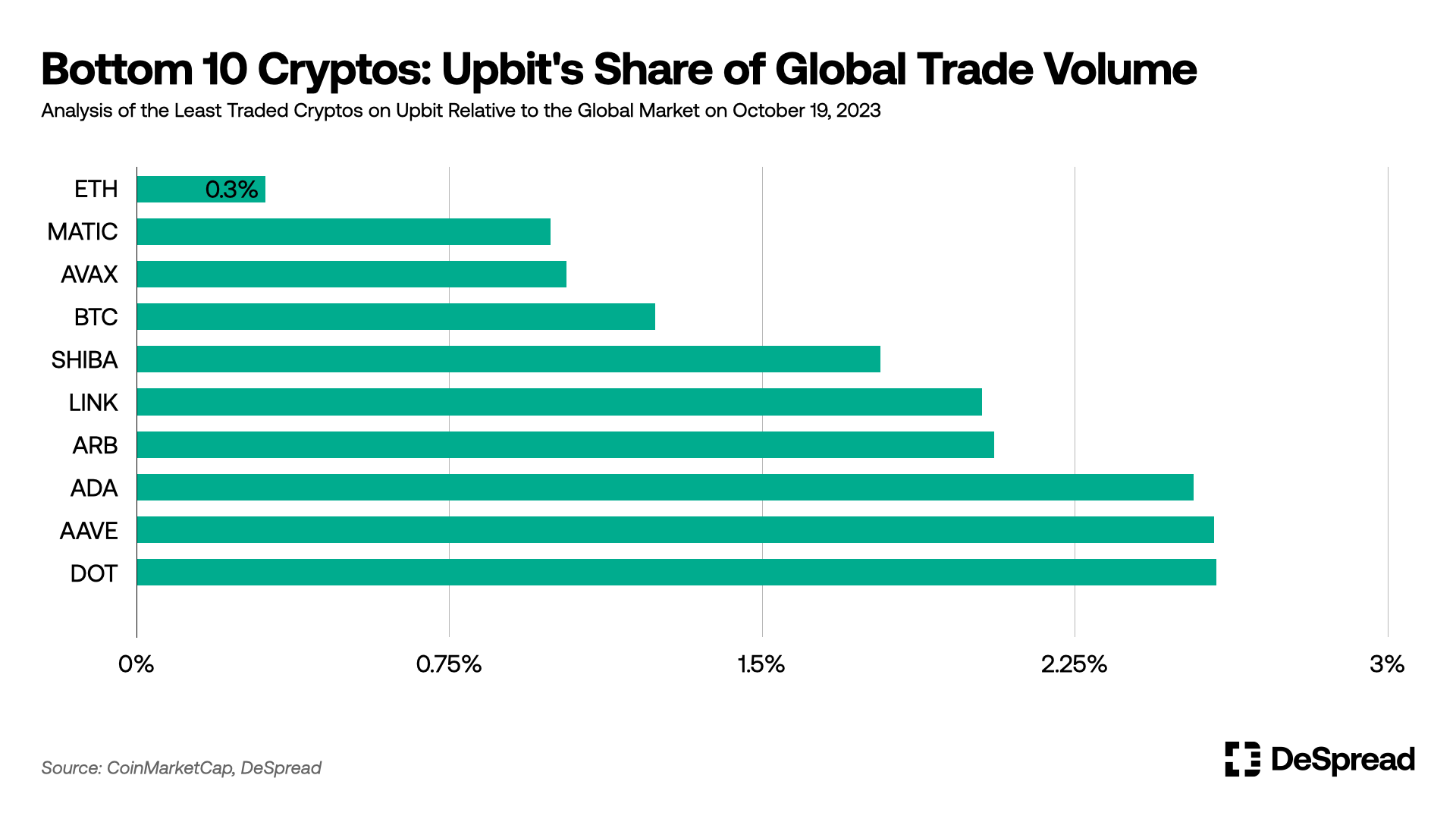

- Relative underperformance of major coins: Cryptocurrencies that dominate the global market, such as Bitcoin (BTC), Ethereum (ETH), and Polygon (MATIC), boast large trading volumes worldwide. However, within Upbit, their trading volume shows surprisingly low levels. This phenomenon indicates that Upbit has unique characteristics compared to the global market and reflects regional disparities in investor preferences and investment strategies. However, it should be noted that Upbit's total trading volume is relatively low compared to giant global exchanges like Binance, so the low trading volume of these major cryptocurrencies should also be taken into account.

- Global trends and diversity of regional markets: As mentioned above, the Korean market exhibits uniqueness compared to the global market, and this is likely to apply to other regions as well. It suggests that global cryptocurrency projects need to establish and implement customized Go-to-Market (GTM) strategies tailored to each regional characteristic.

8. Analysis of Upbit's Deposit and Withdrawal Network

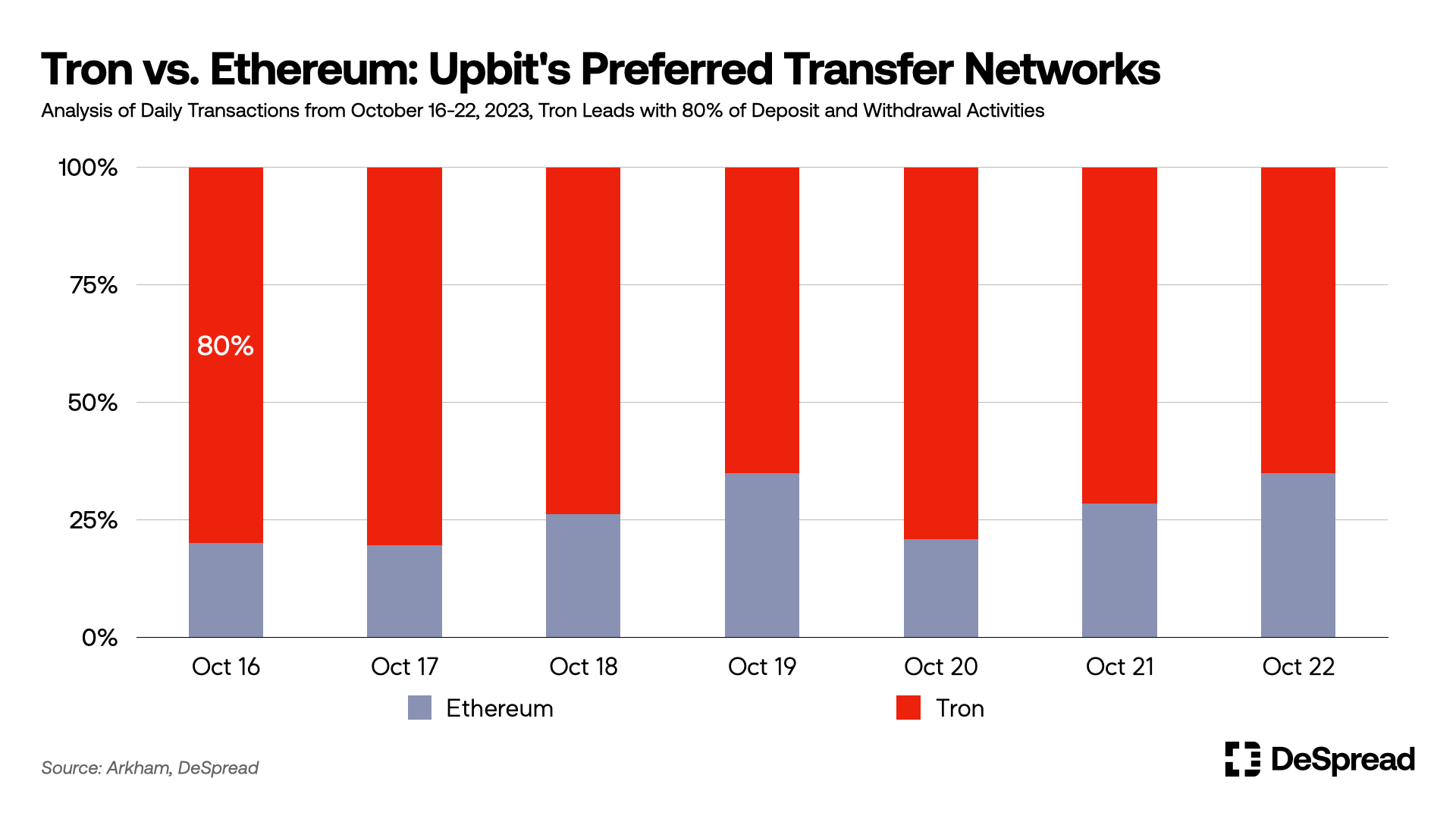

- Upbit users prefer Tron network for deposits and withdrawals: The chart above shows the ratio of transactions between the Ethereum and Tron networks that Upbit users have been using for deposits and withdrawals over the past week. Looking at the data, it shows that the number of transactions on the Tron network trumped those on Ethereum by the factor of 5.

- Tron network gaining popularity with low fees: Upbit users tend to actively use the Tron network for deposits and withdrawals compared to Ethereum. This is because transaction fees on the Ethereum network are relatively high, while Tron network provides low fees and fast transaction processing speed. According to Coinmetrics data, the number of USDT transactions through Tron network reaches up to 2 million per day, while Ethereum only reaches around 100,000 transactions, indicating that the Tron network has a significant advantage in simple fund transfer transactions globally. This phenomenon is also evident in the deposit and withdrawal trends of Upbit users and Korean investors.

- Playing a role as a fiat exchange?: In addition to the above reasons, considering that the Ethereum network has the highest TVL and the most on-chain protocols, it can be interpreted that the purpose of deposit and withdrawal for Korean investors is more about transferring funds between overseas centralized exchanges and Korean exchanges rather than using on-chain products. Various reasons can be suggested for this investor preference, but two main reasons can be considered:

- Originating from the characteristics of Korean investors: Upbit users and Korean investors primarily use exchanges for crypto trading, and they use cryptocurrency deposit and withdrawal services to access products offered by overseas exchanges that are not available on Korean centralized exchanges, such as futures markets and margin trading.

- Originating from convenience differences in on-chain deposit and withdrawal services: Users who want to deposit and withdraw to on-chain environments may prefer withdrawal to the on-chain environment after sending funds to overseas exchanges due to the lack of services provided by Korean centralized exchanges. The lack of services can include the absence of handling stablecoins in dollars and the lack of diversity in withdrawal networks.